Home insurance and home warranty…they sound similar and even seem like they mean the same thing, but there are actually some pretty big differences.

Read on to learn more about some of the bigger differences between home insurance and home warranty plans and how they could be beneficial to you and your property.

Let’s start with the basics.

Home insurance provides coverage for:

- Your structure(s), such as your home, garage, deck, sheds, etc.

- Your personal belongings, such as furniture, clothing and jewelry (subject to individual policy limitations)

- Your liability, which covers damages to others for which you are liable

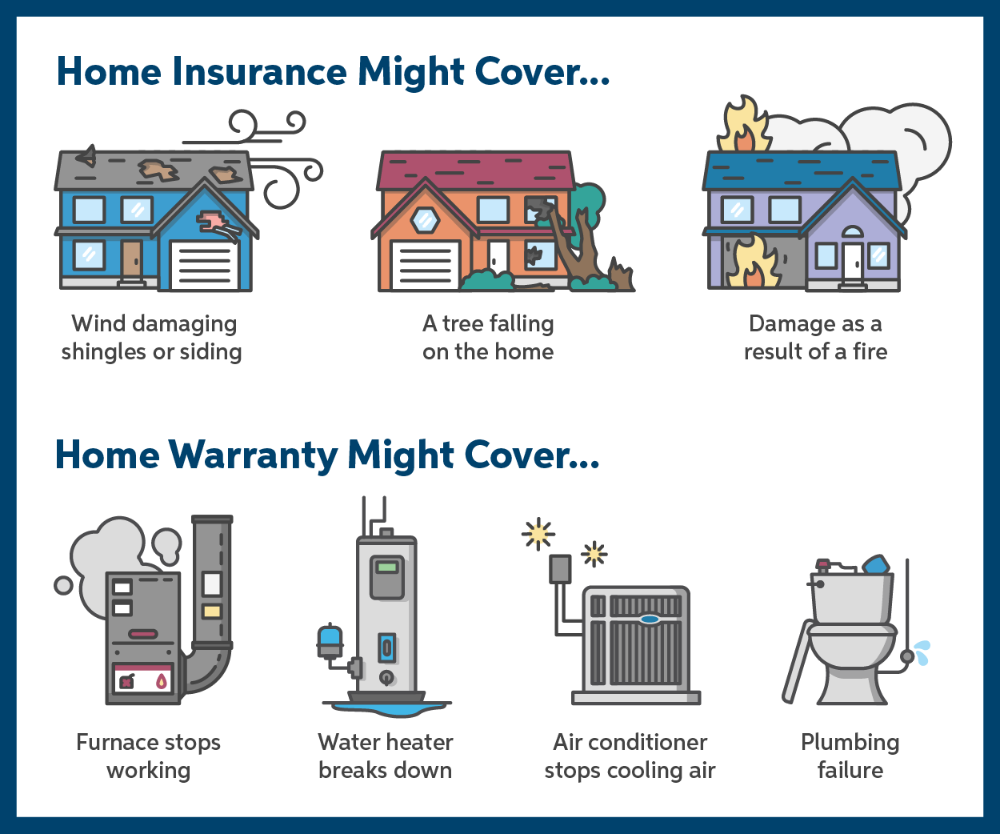

One thing that is not typically covered by a basic home insurance policy is “wear and tear.” This can be confusing as many would assume that if an item wears out, it will be covered by their insurance. But, for insurance, the damage needs to be “sudden and accidental,” such as wind, tree and fire damage.

damage needs to be “sudden and accidental,” such as wind, tree and fire damage.

Some insurance carriers offer add-on coverages that can be applied to a basic home insurance policy, which can cover some types of “wear and tear” exposures. Home insurance and its coverages can vary greatly from company to company or even policy to policy. Working with an independent agent will help ensure that all the coverages you need are added to your policy.

So, what does a home warranty cover?

A home warranty usually covers damages to appliances and home systems that can be expected such as:

- Furnace stops working

- Water heater breaks down

- Air conditioner stops cooling air

- Plumbing failure

Unlike home insurance, a home warranty does not cover the actual home or structures at the location despite the name sounding like it’s a warranty for the home itself. Rather, it’s usually a warranty for certain things that are inside or a part of the home.

There are instances where coverage could overlap between home insurance and a home warranty – especially if a home insurance policy has special coverages added to it. For example, say you have a basic home insurance policy and a basic home warranty as well – if your furnace is old and stops working, it could be covered by the home warranty since it was old and expected to have issues.

However, let’s say that because the furnace died, your pipes accidentally froze and there was water damage to your home. This water damage, since it was sudden and accidental, could be covered by your home insurance policy. If optional coverages have been added to the home insurance policy, the whole event may be able to be covered by that policy alone.

We get it. It’s confusing. To help illustrate these differences, here’s a handy graphic:

Coverage limits for both home insurance and home warranty policies vary depending on individual needs. A larger house with complex home systems may need higher limits than a smaller home with minimal home system exposures.

Coverage limits can have a large impact on overall premiums, so individual policies and plans should be reviewed closely by an agent and the customer to be sure that the right protection is in place.

When in doubt, call your local, Bolder Insurance independent agent.

They’re here to make insurance simple.

Recent Comments